Insights

The CDF Blog

Private lending strategy, market updates, and practical guidance for California borrowers and investors.

April 13, 2026

Breaking Down Fix-and-Flip Financing: Hard Money vs Private Lending

The terms "hard money" and "private lending" get used interchangeably — and that confusion still costs investors money. Understanding the difference in 2026 …

Read more →

April 10, 2026

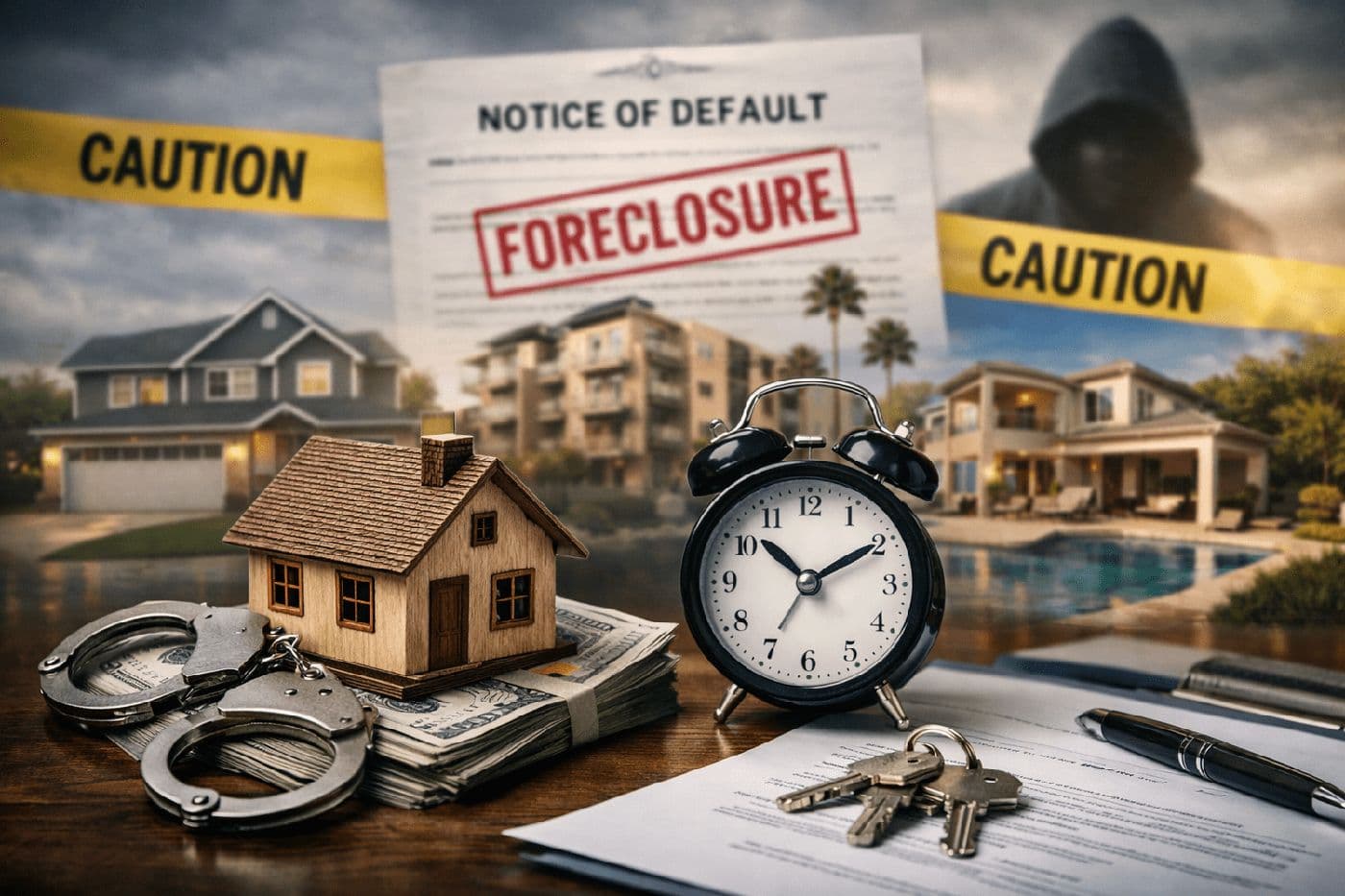

Hard Money vs. Bank Lending – Why Private Capital Is the Foreclosure Solution in 2026

The foreclosure clock doesn't wait for a bank's underwriting committee. And in 2026, that clock is moving faster than it has in years. Foreclosure filings su…

Read more →

April 9, 2026

Sector Spotlight: Why Multifamily, Industrial, and Build-to-Rent Command Capital in 2026

Construction lenders are not distributing capital evenly — and in 2026, that gap is widening. Three property types are absorbing the lion's share of new debt…

Read more →

April 6, 2026

From Application to Closing: Your Blanket Loan Timeline with Capital Direct Funding

Time kills deals in real estate. That's why we've engineered our blanket loan process to move at the speed of opportunity while maintaining thorough underwri…

Read more →

April 1, 2026

Why Brokers and Advisors Choose CDF for Foreign National Clients

Serving foreign national clients in the U.S. real estate market isn't a niche anymore — it's a growing segment that demands specialized financing solutions. …

Read more →

March 23, 2026

Breaking Down California's ADU Laws for 2026: What Homeowners Need to Know

California has been at the forefront of ADU legislation for nearly a decade, and 2026 represents the most enforcement-driven overhaul yet. Where earlier refo…

Read more →

March 20, 2026

DSCR Loans as Your Bridge Loan Exit Strategy

Bridge loans are short-term tools — typically 12 to 24 months. Selling is one exit. In 2026, the smarter play for buy-and-hold investors is refinancing into …

Read more →

March 18, 2026

The LTV Calculator: How Much Can You Actually Borrow in 2026?

The million-dollar question hasn't changed. "How much can I borrow?" What has changed is everything around it. With the 10-year Treasury sitting near 4.2%, t…

Read more →

March 11, 2026

They Say Time is Money – In Foreclosure, It's the Only Thing That Saves Your Home

They say time is money, but in foreclosure, time isn't just money — it's the only thing that can save your home. Every week without financing brings the auct…

Read more →

March 9, 2026

Loan-to-Cost vs. Loan-to-Value – Understanding the Leverage Metrics That Matter

When developers sit down to structure a ground-up construction deal, two numbers shape everything: Loan-to-Cost (LTC) and Loan-to-Value (LTV). Both measure l…

Read more →

March 6, 2026

Case Study: How Capital Direct Funding Solved Complex Portfolio Challenges

Real-world success stories demonstrate the power of creative blanket loan structuring. Here's how we helped three different investors overcome unique portfol…

Read more →

February 28, 2026

Probate Loans in California: What They Are and Why They Matter in 2026

Losing a loved one is hard enough. The last thing any family needs is a 12- to 24-month financial freeze while the courts sort through an estate. ut that's e…

Read more →

February 25, 2026

Backyard or Cash-Yard? Turning Clutter into Cash Flow

Look at your backyard right now. What do you see? If you're like most Southern California homeowners, it's patchy grass, a rusting patio set, and maybe a tra…

Read more →

February 19, 2026

California RUPA and the 120-Day Buyout Rule: Understanding Partnership Dissolution

California's Revised Uniform Partnership Act (RUPA) contains a provision that can destroy business partnerships faster than any market downturn or economic c…

Read more →

February 12, 2026

Waiting for a Construction Draw – Like Watching Paint Dry (With Bills Due)

Every developer knows the cycle. You’ve hit a milestone. The framing is up, MEP is roughed in, or the slab has cured. You’ve submitted the draw request with …

Read more →

February 9, 2026

Blanket Loan Myths Debunked: No, You Won't Lose Everything If You Sneeze Wrong

The internet loves a good horror story, and blanket loans have somehow become the financial equivalent of urban legends. Let's separate fact from fiction bef…

Read more →

February 6, 2026

Foreign Income Documents – Why Lenders Feel Like Translators and Detectives

Open a foreign national loan file and you'll feel it right away. Bank statements in three languages. An accountant's letter that looks nothing like what you'…

Read more →

February 4, 2026

Self-Employed Mortgage Checklist: What You'll Need in 2026

With mortgage rates stabilizing around 6% and non-QM loan options expanding, 2026 presents real opportunities for self-employed borrowers who come prepared. …

Read more →

February 3, 2026

AB 2016 Explained – How California's New Probate Law Impacts Families

Assembly Bill 2016 (AB 2016), effective April 1, 2025, introduced sweeping reforms to California's probate system designed to help families settle estates fa…

Read more →

January 31, 2026

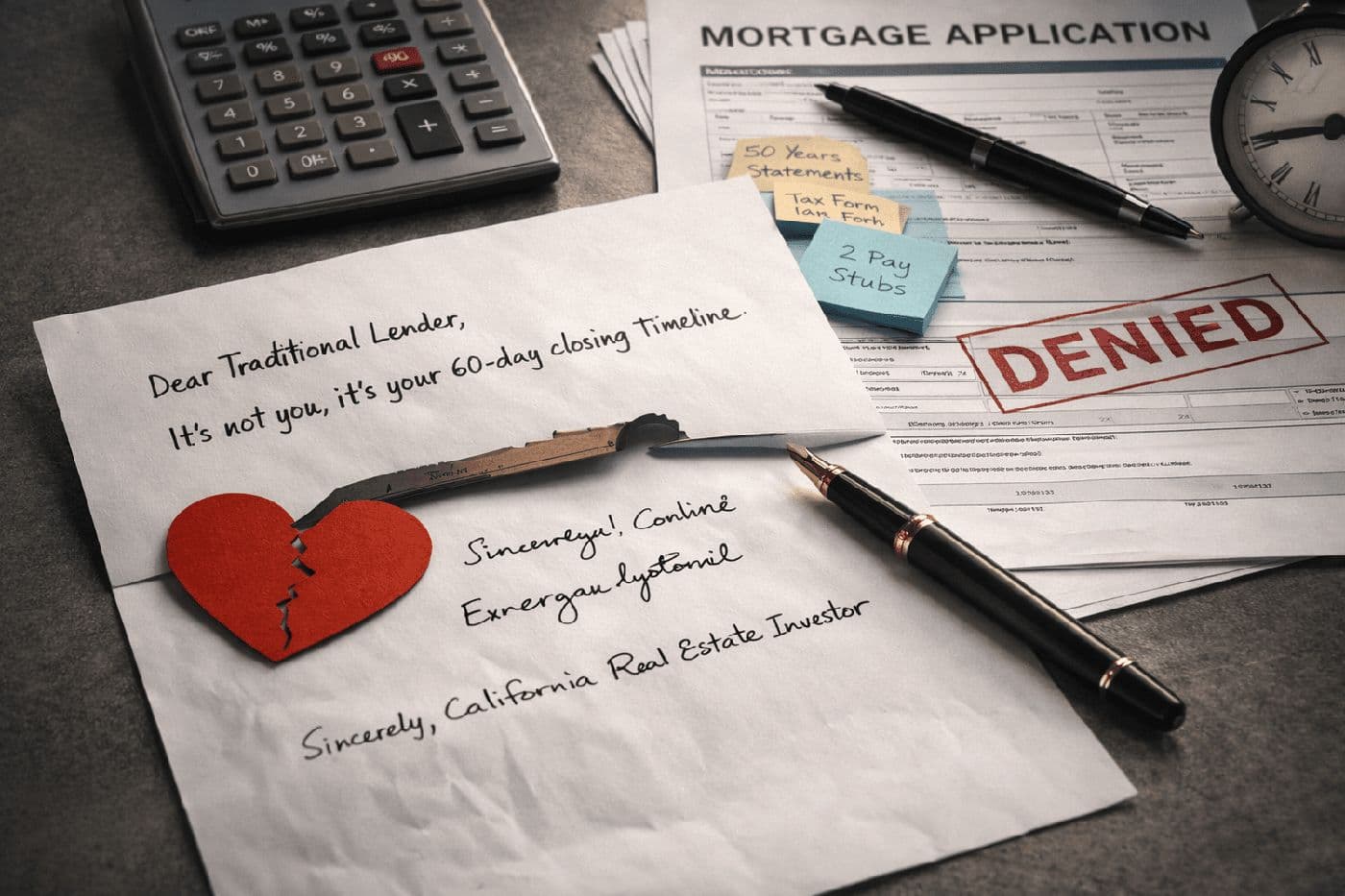

Dear Traditional Lender: It's Not You, It's Your 60-Day Closing Timeline

Dear Traditional Mortgage Lender, We need to talk. This isn't working anymore. It's not you—wait, actually, it is you. It's definitely you. Remember when you…

Read more →

December 22, 2025

From Application to Funding: Our 7-Day Promise for Distressed Properties

When your property is in distress, every day costs money. Late payments accumulate, opportunities disappear, and stress compounds. That's why Capital Direct …

Read more →

December 19, 2025

The Bankruptcy Filing Olympics: When Chapter 11 Becomes an Extreme Sport

Welcome to the 2024 Bankruptcy Filing Olympics, where businesses compete for gold medals in financial creativity, silver medals in survival tactics, and bron…

Read more →

December 17, 2025

California Community Property Laws: How Business Assets Get Divided in Divorce

When business owners in California contemplate divorce, they often assume their enterprise will remain intact. After all, they built it, they run it, and the…

Read more →

December 15, 2025

Bay Area Exodus: Why Everyone's Moving to Fresno (And Loving It)

The great California migration is real, and it's reshaping the entire state's real estate landscape. While San Francisco loses residents, cities like Fresno,…

Read more →

December 12, 2025

The Typical Borrower Profile: Equity-Rich, Credit-Challenged Homeowners

When we picture a homeowner facing foreclosure, the stereotype is often one of financial negligence. The truth? The typical borrower seeking foreclosure fina…

Read more →

December 10, 2025

Why Private Lending Beats Banks for Ground-Up Construction Financing

In the fast-paced world of real estate development—especially in high-stakes, high-opportunity markets like California—the difference between a stalled conce…

Read more →

December 8, 2025

Exit Strategies with Blanket Loans: Planning Your California Portfolio Evolution

The best blanket loan isn't just about today's financing—it's about tomorrow's opportunities. Smart investors structure their blanket loans with clear exit s…

Read more →

December 5, 2025

Faster Approvals, Flexible Solutions – Why Private Lending Works for Foreign Nationals

In today’s dynamic real estate market, speed and adaptability aren’t just advantages—they’re necessities—especially for foreign national borrowers. Internati…

Read more →

December 3, 2025

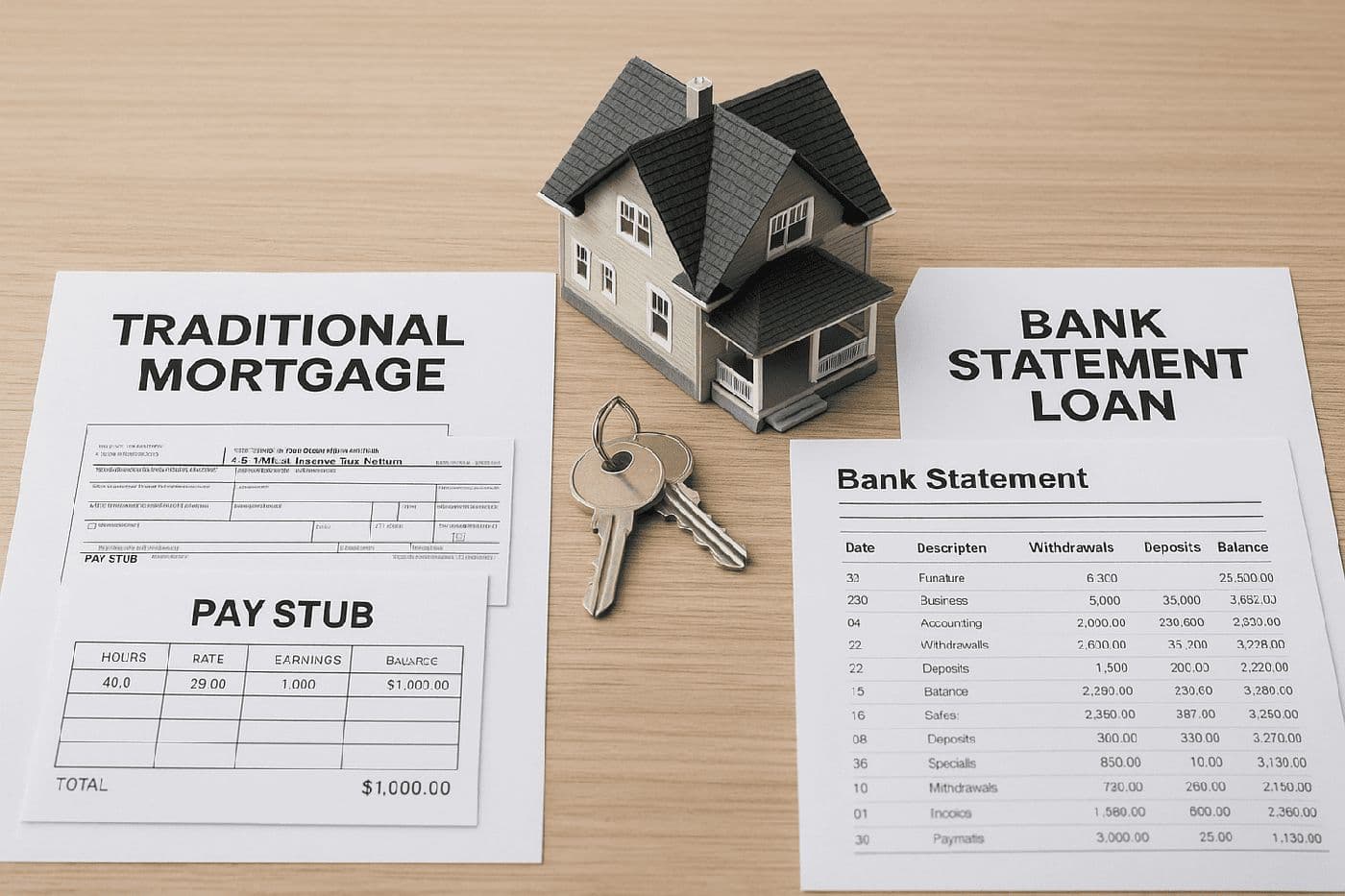

Bank Statement Loans vs Traditional Mortgages: Which Works Better for California Entrepreneurs?

Traditional mortgages and bank statement loans serve the same purpose – helping you buy a home – but they approach income verification from completely differ…

Read more →

December 1, 2025

Money Doesn’t Grow on Trees—But It Might in Probate Loans

Let’s be real: money definitely doesn’t grow on trees. But if you’ve ever waited—and waited—for an estate to settle, you know that accessing inherited assets…

Read more →

November 28, 2025

From Application to Approval – CDF’s Step-by-Step ADU Loan Process

Accessory Dwelling Units (ADUs) are no longer just backyard cottages—they’re powerful financial tools. In California alone, over 30,000 ADU permits were issu…

Read more →

November 27, 2025

The Property That Got Away: Horror Stories from Investors Who Waited Too Long

Gather 'round, California investors, for tales of real estate woe that'll make you clutch your property deeds and whisper, "There but for the grace of bridge…

Read more →

November 24, 2025

The BRRRR Strategy in California's Current Market: Still Viable?

Buy, Rehab, Rent, Refinance, Repeat – the BRRRR strategy built countless real estate portfolios during the low-rate era. But with interest rates above 6% and…

Read more →

November 21, 2025

Understanding DIP Financing: Rates, Requirements, and Strategic Value

Debtor-in-Possession (DIP) financing represents one of the most complex and critical forms of business lending in financial markets. As bankruptcy filings re…

Read more →

November 19, 2025

Business Valuation in Divorce: Income, Market, and Asset Approaches Explained

Business valuation in divorce proceedings is where financial engineering meets legal warfare. Unlike valuations for sale or investment purposes, divorce valu…

Read more →

November 17, 2025

From Application to Funding: What to Expect from Private Lenders

The private lending process remains mysterious to many investors, costing them deals and money. Let's pull back the curtain on exactly what happens from that…

Read more →

November 14, 2025

Waiting for the Bank to Modify Your Loan – Like Waiting for Rain in a Drought

If you’ve ever tried to get your mortgage lender to approve a loan modification, you know it’s less like a business transaction and more like sending message…

Read more →

November 12, 2025

Contractor Delays, Material Costs, and Budget Surprises – Why Financing Feels Like Jenga

Ask any seasoned developer what keeps them up at night, and the answer almost always circles back to two things: contractors and costs . In California’s hype…

Read more →

November 10, 2025

A Day in the Life of Your Properties Under a Blanket Loan

Ever wonder what your properties talk about when you're not around? Here's the exclusive transcript from a recent property portfolio meeting after their owne…

Read more →

November 7, 2025

Foreign National Loans in California: What They Are and Why They Matter

The Financing Challenge for International Buyers While U.S. law allows non-citizens to own property freely, securing a mortgage is far from simple. Foreign n…

Read more →

November 5, 2025

Financing Solutions for California Entrepreneurs: When Tax Strategy Complicates Homeownership

At Capital Direct Funding , we understand a reality many California business owners face: your business may be thriving, but your tax returns don’t always re…

Read more →

November 3, 2025

Probate Lending and Proposition 19: Protecting Property Tax Bases

How Proposition 19 Changed Inheritance Rules California’s Proposition 19, approved by voters in November 2020, significantly altered long-standing property t…

Read more →

October 31, 2025

The True Cost of Building an ADU: Hard Costs, Soft Costs, and Hidden Surprises

Building an Accessory Dwelling Unit (ADU) is an exciting opportunity for homeowners to add rental income, accommodate family members, or increase property va…

Read more →

October 29, 2025

5 Signs You Need a Bridge Loan (Hint: If You're Reading This at 2 AM, That's Sign #1)

We see you there, scrolling through real estate listings at ungodly hours, calculator app open, trying to figure out how to make that perfect investment prop…

Read more →

October 27, 2025

The AB 2424 Advantage: How California's New Law Gives You More Time to Save Your Property

January 1, 2025, marked a seismic shift in California's foreclosure landscape. Assembly Bill 2424 didn't just tweak the process – it fundamentally rewrote th…

Read more →

October 24, 2025

The Great Student Loan Discharge Unicorn Sighting (It Actually Happened!)

In bankruptcy circles, successfully discharging student loans is like spotting a unicorn—everyone's heard stories, but nobody believes they exist. Until 2024…

Read more →

October 22, 2025

Bridge Financing for Divorce: How Capital Direct Funding Solves Your Timeline Crisis

Divorce proceedings operate on crisis time. Court deadlines approach like freight trains, partnership buyouts demand payment in 120 days, and business disrup…

Read more →

October 20, 2025

Why California's Inland Markets Are the Hidden Gems for Fix-and-Flip Success

The California real estate investment landscape has shifted dramatically. While everyone's eyes remain glued to Los Angeles and San Francisco headlines, savv…

Read more →

October 17, 2025

California’s Foreclosure Prevention Laws – Lessons from the Past, Outlook for 2025

A Legacy of Intervention California has long been at the forefront of foreclosure prevention. During the Great Recession, the state enacted pivotal legislati…

Read more →

October 15, 2025

Capital Direct Funding’s Advantage – Supporting Developers in High-Cost Markets

California’s real estate landscape is among the most dynamic—and demanding—in the nation. Soaring land prices, escalating construction costs, tight labor mar…

Read more →

October 14, 2025

Understanding Release Clauses in Blanket Loans: A California Investor's Guide

Release clauses are the Swiss Army knife of blanket loans—versatile, powerful, and absolutely essential for portfolio flexibility. Yet many California invest…

Read more →

October 11, 2025

How Capital Direct Funding Simplifies Foreign National Real Estate Loans—With Service at the Core

Foreign nationals investing in California real estate often face significant hurdles when seeking financing. Traditional lenders typically require U.S. credi…

Read more →

October 8, 2025

Why California Freelancers Choose Private Lending Over Traditional Banks

Traditional banks promise low rates and standardized processes. Yet increasingly, California's freelancers and independent professionals are choosing private…

Read more →

October 6, 2025

How Capital Direct Funding Delivers Fast, Flexible Probate Loans

Navigating probate can be emotionally and financially draining. While the legal process often takes months—or even years—bills don’t pause . Mortgages, prope…

Read more →

October 3, 2025

They Say Money Doesn’t Grow on Trees — In California, It Grows in Backyards

They say money doesn’t grow on trees. In California? It might just grow in your backyard — if you build an Accessory Dwelling Unit (ADU). An ADU — whether it…

Read more →

October 1, 2025

California Assembly Bill 3108: What Real Estate Investors Need to Know About Bridge Loans

California Assembly Bill 3108, enacted recently, significantly impacts bridge lending for real estate transactions. This legislation aims to protect consumer…

Read more →

September 30, 2025

Real Estate Investing Myths Busted: No, You Don't Need Perfect Credit and a Trust Fund

Let's destroy some real estate investing myths that keep regular people from building wealth. Spoiler alert: Your Instagram feed is lying to you, and that gu…

Read more →

September 24, 2025

California's 2024 Bankruptcy Law Changes: What Businesses Need to Know

California's bankruptcy landscape underwent significant transformation in 2024, with legislative changes that fundamentally alter how businesses navigate fin…

Read more →

September 19, 2025

The Top 10 Questions People Ask Us (And the One That Made Us Spit Out Our Coffee)

After years of specializing in divorce buyout financing, we've heard every question imaginable. Some are predictable, some are insightful, and one made our e…

Read more →

September 17, 2025

Central Valley Gold Rush: Market Analysis for Smart Investors

The Central Valley is experiencing its moment, and smart investors are staking claims. While coastal California grabs headlines, the real action—and profits—…

Read more →

September 16, 2025

From Auction to Advantage – How Our Loans Buy You Time and Options

Foreclosure auctions represent one of the most consequential — and irreversible — moments in a homeowner’s financial journey. Once a property sells at auctio…

Read more →

September 12, 2025

Ground-Up Construction – Where Coffee, Cash Flow, and Contingencies Keep You Alive

Ground-up construction isn’t for the faint of heart. It demands relentless energy, unwavering discipline, and deep financial resources. Developers often joke…

Read more →

September 10, 2025

California's 2025 Regulatory Changes: Impact on Blanket Loan Strategies

California's commercial lending landscape shifted significantly in 2025, with new regulations affecting how blanket loans are structured and serviced. Unders…

Read more →

September 9, 2025

Opening California’s Housing Market to Global Buyers

California has long been a magnet for global capital. From its thriving economy to its world-class lifestyle, the state attracts investors, immigrants, and e…

Read more →

September 2, 2025

Prefab vs. Custom ADUs – Complete Financing Guide for 2025

Building an accessory dwelling unit (ADU) can be a smart way to generate rental income, increase property value, or create space for family. But before the f…

Read more →

September 2, 2025

Fix and Flip Financing: How Bridge Loans Fund Your Next California Project

California's fix-and-flip market demands speed, flexibility, and capital—exactly what bridge loans deliver. Traditional banks won't finance distressed proper…

Read more →

August 29, 2025

Banks vs. Private Lenders: A Speed Dating Comparison

Dating apps have nothing on the lending industry when it comes to mismatched expectations and painful rejection. Let's compare your financing options using a…

Read more →

August 28, 2025

DIP Financing: How Capital Direct Funding Navigates California's Complex Bankruptcy Market

When your business enters Chapter 11 bankruptcy, maintaining operations becomes a race against time. Debtor-in-Possession (DIP) financing provides critical c…

Read more →

August 27, 2025

Why Your Bank Runs Slower Than DMV Lines When You Need a Divorce Buyout

Picture this: You're facing a divorce buyout deadline. The court says you have 90 days to fund the settlement. Your partnership agreement demands payment in …

Read more →

August 15, 2025

Navigating California's Self-Employed Financing Maze: Your 2025 Guide to Success

The self-employed economy in California is thriving—but is your access to capital keeping pace? If you're among California's 2.2 million self-employed worker…

Read more →

August 15, 2025

Foreign Buyers Face New Hurdles in California – But Opportunity Still Knocks

The California real estate market is experiencing a fascinating paradox in 2025. Foreign investment is surging – up 44% with $56 billion in purchases nationw…

Read more →

August 15, 2025

5 Critical Insights Every California Fix-and-Flip Investor Needs to Know in 2025

The California real estate market has shifted dramatically in 2025, creating both unprecedented challenges and hidden opportunities for fix-and-flip investor…

Read more →

August 14, 2025

Understanding "Bankruptcy Financing Loans": What California Businesses Really Need to Know

If you've found yourself searching for "bankruptcy financing loans" in California, you're likely facing significant financial challenges. While this term is …

Read more →

August 14, 2025

Navigating Cross-Collateralization and Blanket Loans in California's 2025 Real Estate Market

California's real estate market presents a unique challenge for investors in 2025. With home prices sitting at more than double the national average and mort…

Read more →

August 14, 2025

California Business Buyouts in 2025: Why Smart Financing Can Save Your Deal

Every California business buyout faces the same critical challenge: securing enough capital, quickly enough, to meet legal deadlines without destroying the b…

Read more →

August 14, 2025

California Bridge Loans: Close in Days, Not Months (Perfect for 1031 Exchanges)

That perfect property just hit the market. Your 1031 exchange deadline is approaching. The auction ends tomorrow. While banks need 45 days, you need funding …

Read more →

August 14, 2025

Build California's Future: Ground-Up Construction Loans for Visionary Developers (2025)

Empty lots. Tear-down properties. Underutilized land. While others see vacant space, you see tomorrow's landmarks. In 2025, California's housing shortage has…

Read more →

August 14, 2025

California's Distressed Property Goldmine: Quick Financing for Maximum Returns in 2025

Smart investors know: California's distressed properties are today's best-kept secret. With commercial properties down 40-60% from peaks and residential fore…

Read more →

August 14, 2025

Unlock Your Property's Hidden Potential: The Ultimate Guide to ADU Construction Loans in California (2025)

Picture this: Your California property has untapped potential worth hundreds of thousands of dollars. It's sitting right in your backyard, above your garage,…

Read more →

August 14, 2025

Navigating California's Probate Process: How Estate Loans Can Be Your Financial Bridge in 2025

If you're reading this, chances are you're dealing with one of life's most challenging moments – settling an estate while waiting for probate to conclude. In…

Read more →

August 14, 2025

Los Angeles Homeowners: Stop Foreclosure Now with Capital Direct Funding

The LA Reality Check Los Angeles homeowners are facing a harsh reality. In 2025, 782 foreclosure starts hit LA County in May alone - making it the 4th highes…

Read more →

April 17, 2025

Hudson Pacific Secures $475M in CMBS Financing for West Coast Office Portfolio

Hudson Pacific Properties has secured a $475 million commercial mortgage-backed securities (CMBS) loan, supported by a six-building office portfolio spanning…

Read more →

April 17, 2025

Tech Industry Fuels San Francisco’s Strongest Office Leasing Quarter in a Decade

San Francisco's office market is showing renewed strength, posting its highest leasing activity in ten years as tech companies lead the charge in securing sp…

Read more →

April 17, 2025

3650 Capital Raises $215 Million to Expand Commercial Real Estate Lending Strategies

Commercial real estate investment firm 3650 Capital has secured $215 million from institutional investors to scale its diversified CRE lending strategies. Th…

Read more →

July 20, 2023

How do I find a good commercial property to invest in?

Commercial real estate investing can be a lucrative and rewarding way to diversify your portfolio and generate passive income. However, finding a good commer…

Read more →

July 14, 2023

How AI, Data and Green Will Transform Pro Forma Analysis in Real Estate

Pro forma analysis is a vital tool for real estate investors and developers, as it helps them evaluate the feasibility and profitability of a property or pro…

Read more →

June 9, 2023

You Can Now Buy a Home With Just 1% Down — But Should You Get One of These Bargain Mortgages?

Two of the nation’s largest lenders are now removing the struggle many homebuyers face in saving up for a down payment by offering loans that require just 1%…

Read more →

June 9, 2023

Yikes! Mortgage Rates Just Jumped Again—and Here’s How High They Might Go

Mortgage rates jumped higher this week, further dashing homebuyers’ hopes for an affordable spring home-shopping season. Rates for a 30-year fixed-rate mortg…

Read more →

May 19, 2023

U.S. house prices experience the largest yearly decline since January 2012

Existing-home sales fell to a rate of 4.28 million in April, the National Association of Realtors said The numbers : Sales of previously-owned homes in the U…

Read more →

May 15, 2023

Good News for Homebuyers: Mortgage Rates Are Poised To Fall

Mortgage rates are poised to begin coming down. The U.S. Federal Reserve isn’t expected to announce another interest rate hike in the wake of the banking cri…

Read more →

May 8, 2023

U.S. Home Prices Are Up, Down, and All Over the Place—See How They’re Faring Where You Live

These days, many folks are on edge over the much-feared housing recession—a dread that descended like a dark cloud last year as the real estate market seemed…

Read more →

May 8, 2023

Where Americans Want To Live: These Ultra-Affordable, Up-and-Coming Real Estate Markets

Americans’ bank accounts are under siege. Whether it’s a trip to the supermarket or a night out for dinner and a movie, the cost of just about everything see…

Read more →

April 21, 2023

Mortgage Rates Just Jumped: Will the Spring Real Estate Market Survive?

After a five-week stretch of declines, mortgage rates ticked up this week, sending ripples of dread through an already shaky spring market. For the week endi…

Read more →March 31, 2023

How to Find a Real Estate Agent: Where to Look and What to Ask

Before putting your home on the market or setting out to buy a new one, you should identify real estate agents in your community who can assist with the sale…

Read more →

March 27, 2023

Is This the Calm Before the Mortgage-Rate Storm? Here’s Why Homebuyers Should Hurry

Although the Federal Reserve hiked interest rates on Wednesday, mortgage rates veered in the opposite direction and tumbled. For the week ending March 23, th…

Read more →

March 13, 2023

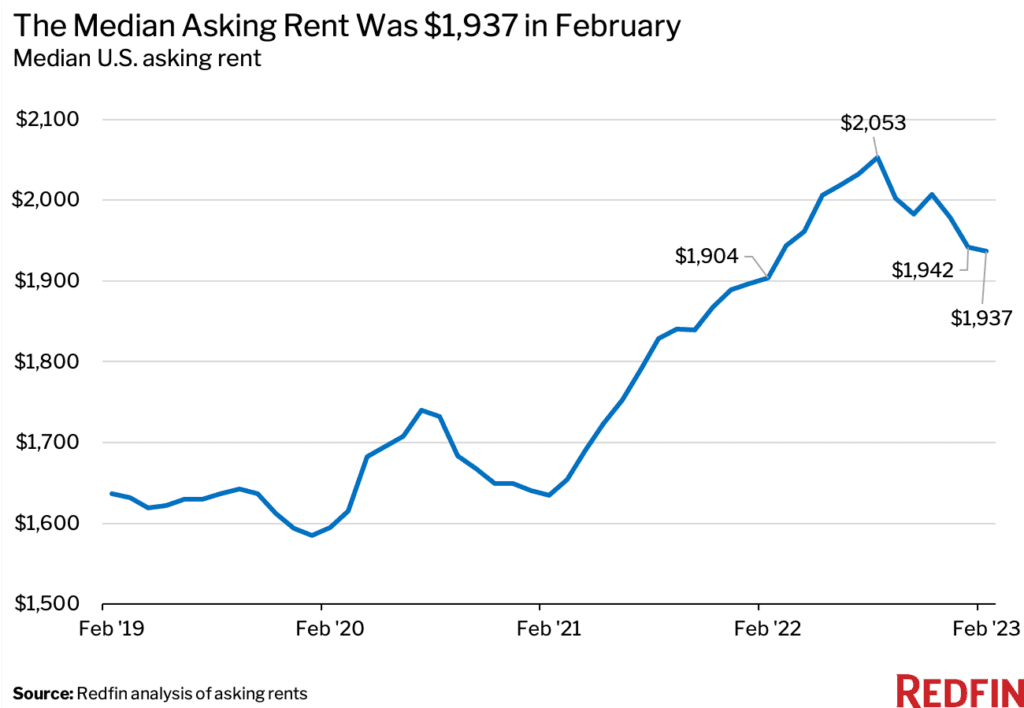

Rental Market Tracker: Rents Drop To Lowest Level In A Year

The median U.S. asking rent is up just 1.7% from a year ago—the smallest gain since May 2021—as landlords grapple with vacancies due to still-high rental cos…

Read more →

March 6, 2023

Homebuyers Beware: You Might Have To Pay More Property Taxes Than You Think

Price is one of the most critical factors in buying a home. But there’s something else you need to consider when budgeting for a new house: property taxes . …

Read more →

February 27, 2023

U.S. New-Home Sales Rise by 7.2% Despite Weakness in the Broader Sector

The numbers: U.S. new-home sales rose 7.2% to a seasonally adjusted rate of 670,000 in January, up from a revised 625,000 in the prior month, the Commerce De…

Read more →

February 20, 2023

How To Calculate Property Tax: What Homeowners Should Know About How to Estimate Property Taxes

Most people know that homeownership requires coughing up copious amounts of money. There’s your mortgage , of course, but the costs hardly end there. What ab…

Read more →

February 14, 2023

Seller’s Market, Buyer’s Market, ‘Nobody’s Market’? The Weird State of Housing Right Now

Today’s housing market has everyone wondering: Is it still a seller’s market , or has the power dynamic finally shifted in favor of buyers? Try neither. Unce…

Read more →

February 6, 2023

What Is a Multifamily Home? Owning Many Units Can Lead to a Steady Cash Flow

Unlike single-family homes, multifamily homes are dwellings with more than one unit that each have their own bathroom and kitchen. Interested in how this typ…

Read more →

January 30, 2023

Housing Market Update: Sales Are Slow To Kick Off New Year, But More Buyers Start Searching

Homes are selling at their slowest pace since the housing market nearly ground to a halt at the beginning of the pandemic. The typical home that sold during …

Read more →

January 23, 2023

How Long Does It Take to Build Credit History From Scratch?

If you ever plan to buy a house, establishing a track record of past payments is essential, because it proves to mortgage lenders that you’ve paid people bac…

Read more →

January 16, 2023

Can You Show Your Home With an Offer on the Table?

Can you show your home with an offer on the table? Sure, you’ve found a (nearly) perfect buyer. You’ve accepted the offer , which means you’re in wedded blis…

Read more →

January 9, 2023

2023: The Year of the Homebuyer? Our Bold Predictions on Home Prices, Mortgage Rates, and More

It’s safe to say we’ve never encountered a housing market nearly as unpredictable as the one we’re in right now. After months of navigating wild fluctuations…

Read more →

October 10, 2022

Mortgage Rates Dip Slightly to 6.66%, but Have Doubled From a Year Ago

T he numbers: Mortgage rates took a breather from its march towards 7% this week, as the economic outlook looks uncertain . The 30-year fixed-rate mortgage a…

Read more →

September 27, 2022

Mortgage Rates Rise for Fifth Week in a Row, Hitting 6.29%

By Charley Grant Sep 22, 2022 Mortgage rates rose for the fifth consecutive week, reaching yet again the highest level since the financial crisis. The averag…

Read more →

September 27, 2022

US Housing Prices Fall for First Time Since 2012

Pandemic frenzy is hitting the skids as mortgage rates climb Index of 20 cities posts first monthly decline since 2012 Say goodbye to the housing bull run. U…

Read more →

July 31, 2019

Rodolfo Campos and Diego Corona Affordable Homeownership Interns 2019 .

What interested you most about an Internship at Capital Direct Funding? Rodolfo Campos: Taking on challenges is something that I have embraced my entire life…

Read more →

March 12, 2019

Want to Grow? Join me March 14th!! NAHREP LA San Gabriel Valley Event. Real Estate, Build Your Future.

Sandra Williams is President and Co-Founder of Capital Direct Funding in West Covina, California and now Marketing Director for NAHREP San Gabriel Valley. Sh…

Read more →

October 4, 2018

Commercial Closing!

Capital Direct Does Commercial! Hey there everyone! Its the beginning of the final quarter of the year. We constantly want to share with you valuable informa…

Read more →

September 20, 2018

National Mortgage Professional : Featured Industry Leader

Read more →

March 28, 2018

CDF Easter Blessings 2018

In 2017 Capital Direct Funding began the Easter Blessings Campaign. This thoughtful project came about through Frank Williams, Divisional Manager of CDF. Fra…

Read more →

March 14, 2018

Relieve stress and increase productivity through exercise with Sandra Williams

“Where we put our time reflects our deepest values” states Sandra Williams, Co- founder and President of Capital Direct Funding. The key to balancing your li…

Read more →

March 1, 2018

2018 Gubernatorial Forum Candidates

A year ago I was asked to serve as the Los Angeles Chair of an organization called THE 200 led by Joe Coto former California State Assemblyman and John Gamb…

Read more →

January 9, 2018

The Latina Global Executive Leadership Program and My 2018 Advisor Role

A year ago I was given the opportunity to embark on an incredible journey to grow my education in a way I had thought unimaginable. Due to my active communit…

Read more →

March 30, 2017

Did you know we can help your clients with tax issues still accomplish their real estate goals?

Are your clients facing these problems? ● Reduced profits from the previous filing year ● Problems seeking access to capital ● Need to compare…

Read more →

March 22, 2017

Are your self-employed clients having trouble qualifying for a real estate loan?

Develop a more inclusive pre-screening prospecting questionnaire by including private money criteria!! Door-knocking is a great prospecting activity to incre…

Read more →

March 16, 2017

Do you have clients who are in Probate?

Taking a case to probate court can be an expensive, lengthy, and complex process. At Capital Direct Funding, we are the experts at probate and crisis situati…

Read more →

March 8, 2017

Poor Credit History

Poor Credit History : Finding a home loan with poor credit history can be challenging.It is important to know alternative financing options for your borrower…

Read more →

February 28, 2017

New Year , New Startup , but don’t have the 2 year financial minimum?

Get them closed now, with Private Money! Spring into Action!! Start closing millennial startups who have the capacity to purchase properties, but have not be…

Read more →

February 21, 2017

Having trouble closing escrow on time? Time is ticking! you still have time to close by the end of the month!!!

Don’t you dislike when Doc’s were supposed to go out this morning and did not?? There must be issues in the file. Let us be your backup on your files that ma…

Read more →

February 15, 2017

Did you know we can help your clients who do not have seasoned funds?

Unexpected things often come up in the loan process!!! Many mortgage lenders today require funds to be seasoned. They require a minimum of 60 days or more fo…

Read more →

February 9, 2017

Do you have self-employed borrowers who are struggling to obtain cash for expanding their rental properties business?

If your self-employed borrowers have multiple properties, good credit score, good financial situations and paying mortgage on time but are struggling to obta…

Read more →

February 1, 2017

Are your buyers having trouble using the seller’s equity as a gift to Purchase a Property? If your answer is yes, We can help!

Using equity can help people buy a property. If your sellers are thinking of selling a property with high equity to a family member or friend and the buyers …

Read more →January 26, 2017

Don’t Cast the Net Too Shallow!

Door knocking, Prospecting Mistakes lol Door-knocking is a great prospecting activity to increase your customers. Through this process, key pre-screening que…

Read more →

January 18, 2017

Client was pre-approved, then……?

Employment status changed? Purchased a brand-new car as a Christmas gift? Income changed? Bought new furniture early? Signed up for a new credit card? Nothin…

Read more →

January 11, 2017

Are your clients having trouble getting a loan? We can help!

We are the experts at turning a complex issue into a simple solution... Requirements for conventional financing can be difficult for people who have non-trad…

Read more →

December 21, 2016

There Is No Such Thing As A Cosigner!

At Capital Direct Funding, we want to help you and your clients through their challenging mortgage situations. We want to hear your story, so that we can ana…

Read more →

December 16, 2016

Complex Situations? No problem!!

Have your clients been turned down from other lenders? Meet Matt-Real Estate Attorney. His client is Jessica. She has a very complex legal battle. She is try…

Read more →

December 8, 2016

We're Not Like the Other Lenders

Capital Direct Funding, we are a private money lender facilitating loans for individuals who aren't qualified through traditional banks. Instead of a long an…

Read more →

November 30, 2016

Low Credit Score

“My credit score is 550. Can I get a home loan with such a low score?” “ Do I need to boost my credit score to get home loan?” “ My credit score wasn't quali…

Read more →

November 2, 2016

We welcome ITIN customers

Foreign Nationals At Capital Direct Funding, we can help improve your business from good to great and help your clients reach their real estate goals. Owning…

Read more →

October 27, 2016

No More Runaround!

When you're looking to prequalify for a mortgage and the majority of your income is from being a 1099 independent contractor, many lenders will evaluate your…

Read more →

October 12, 2016

Save your home from Tax Sale!

Do you find yourself asking these questions? “I received a “Notice of Sale” for my Property Taxes, What should I do?” “I couldn’t pay my property taxes and m…

Read more →

October 5, 2016

Access to Capital for the Self-Employed, Finally!

When you're self-employed, taking out a loan can feel like searching for a needle in a haystack. Banks give you the runaround for days asking for a multitude…

Read more →

September 26, 2016

We efficiently help your clients deal with tax issues!

Are your self employed clients facing these problems? ● Reduced profits from previous filing year? ● Filed an extension instead of filing tax? ● Having probl…

Read more →

September 16, 2016

We help your clients whom are in Probate!

Are your clients facing situations like? Needing Money for Attorney's Fee? Needing Money to repair their property? Needing Money for tenant issues? Foreclosu…

Read more →

September 7, 2016

Issues with Closing? Capital Direct Funding Can Help!

Unexpected delays in acquiring your investment is always disheartening. Here are a few common problems that arise during the loan process for a real estate p…

Read more →

August 17, 2016

How to save file turn downs?

Did your escrow fall out? What are some of the reasons why escrow would fail? Getting an offer accepted can seem like the easy part these days. Getting the e…

Read more →

August 10, 2016

How to get into Escrow

How to Get Into Escrow! As a Real Estate or Mortgage Professional, we understand the myriad of challenges that you face in qualifying your buyers. In fact, w…

Read more →

March 25, 2015

What’s Ahead For Mortgage Rates This Week – April 27, 2015

Last week’s housing related reports included the FHFA Home Price Index, the National Association of Realtors® Existing Home Sales report and The Commerce Dep…

Read more →

February 23, 2015

The Three Essential Habits That Successful Home Buyers Must Embrace

Whether you are preparing to purchase your investment property or it has been many years since you last walked through the home buying process, you may be st…

Read more →Capital Direct Funding

We couldn't find the page you were looking for. This is either because: There is an error in the URL entered into your web browser. Please check the URL and …

Read more →Capital Direct Funding

We couldn't find the page you were looking for. This is either because: There is an error in the URL entered into your web browser. Please check the URL and …

Read more →