Homes are selling at their slowest pace since the housing market nearly ground to a halt at the beginning of the pandemic. The typical home that sold during the four weeks ending January 8 was on the market for 44 days, the longest timespan since April 2020, contributing to the biggest annual inventory increase on record. Pending home sales dropped 32% year over year to their lowest level on record and mortgage-purchase applications dropped to their lowest level since 2014.

High mortgage rates and extreme winter weather at the start of the year deterred would-be homebuyers, exacerbating the typically holiday slowdown. But there are signs that early-stage demand is up. Redfin’s Homebuyer Demand Index–a measure of tour requests and other buying services from Redfin agents–posted a 6% increase over the last month, and Google searches for “homes for sale” are on the rise. Some buyers are likely coming in from the sidelines because mortgage rates have dropped to 6.33% from their November peak of over 7%, saving the typical U.S. homebuyer roughly $250 on monthly housing payments.

Buyers may also be encouraged by signs of improvement in the economy, with inflation easing in December for the sixth month in a row as wage growth softens.

“We’re entering 2023 with positive economic news: The latest consumer price index report confirms that the worst of inflation is behind us. That means the Fed is likely to continue easing its interest-rate increases, which should cause mortgage rates to continue gradually declining. This could bring back some homebuyers in the coming months,” said Redfin Deputy Chief Economist Taylor Marr. “We’ve already seen an uptick in people initiating home searches. Although those house hunters haven’t yet turned into buyers, they may soon given that monthly mortgage payments are notably down from their peak and the latest inflation and employment data lower the chances of a recession.”

Home prices fell from a year earlier in 20 of the 50 most populous U.S. metros

The typical U.S. home sold for $351,250 during the four weeks ending January 8. That’s up 0.8% from a year earlier, but down about 10% from the June peak.

Home-sale prices fell year over year in 20 of the 50 most populous U.S. metros. By comparison, 11 metros saw price declines a month earlier.

Prices fell 10.6% year over year in San Francisco, 5% in Seattle, 4.9% in San Jose, 4% in Austin, 3.8% in Detroit, 3.7% in Phoenix, 3.4% in Oakland, CA, 3% in Boston, 3% in Los Angeles, 3% in Sacramento, 2.6% in San Diego and 2.5% in Chicago. They fell 2% or less in Portland, OR, Anaheim, CA, Portland, OR, Riverside, CA, Newark, NJ, New York, Pittsburgh, Las Vegas and Washington, D.C.

This marks the first time Las Vegas prices have dropped year over year since at least 2015. It’s the biggest year-over-year price drop in San Francisco, Seattle, Phoenix, Chicago, Boston, Portland and San Diego since at least 2015.

Leading indicators of homebuying activity:

For the week ending January 12, 30-year mortgage rates declined from the week before to 6.33%. The daily average was 6.15% on January 11.

Mortgage-purchase applications during the week ending January 6 declined 1% from a week earlier, seasonally adjusted, hitting their lowest level since 2014. Purchase applications were down 44% from a year earlier.

The seasonally adjusted Redfin Homebuyer Demand Index–a measure of requests for home tours and other homebuying services from Redfin agents–was essentially flat from a week earlier and up 6% from a month earlier during the four weeks ending January 8. It was down 29% from a year earlier.

Google searches for “homes for sale” were up nearly 50% from their November low during the week ending January 7, but down about 17% from a year earlier.

Key housing market takeaways for 400+ U.S. metro areas:

Unless otherwise noted, the data in this report covers the four-week period ending January 8. Redfin’s weekly housing market data goes back through 2015.

Data based on homes listed and/or sold during the period:

The median home sale price was $351,250, up 0.8% year over year.

The median asking price of newly listed homes was $352,150, up 3.9% year over year.

The monthly mortgage payment on the median-asking-price home was $2,263 at the current 6.33% mortgage rate. That’s roughly flat from a week earlier and down $244 from the October peak. Monthly mortgage payments are up 32.7% from a year ago.

Pending home sales were down 31.7% year over year to the lowest level on record, the 12th straight period of pending sales declining more than 30%.

Among the 50 most populous U.S. metros, pending sales fell the most in Las Vegas (-61.9% YoY), Jacksonville, FL (-57.4%), Phoenix (-56.9%), Austin, TX (-55.3%) and Nashville (-50.8%).

New listings of homes for sale fell 21.9% year over year.

Active listings (the number of homes listed for sale at any point during the period) were up 20.7% from a year earlier, the biggest annual increase since at least 2015.

Months of supply—a measure of the balance between supply and demand, calculated by dividing the number of active listings by closed sales—was 3.8 months, up from 3.4 months a week earlier and up from 1.9 months a year earlier.

27% of homes that went under contract had an accepted offer within the first two weeks on the market, down from 34% a year earlier.

Homes that sold were on the market for a median of 44 days, the longest time period since April 2020. That’s up nearly two weeks from 31 days a year earlier and the record low of 18 days set in May.

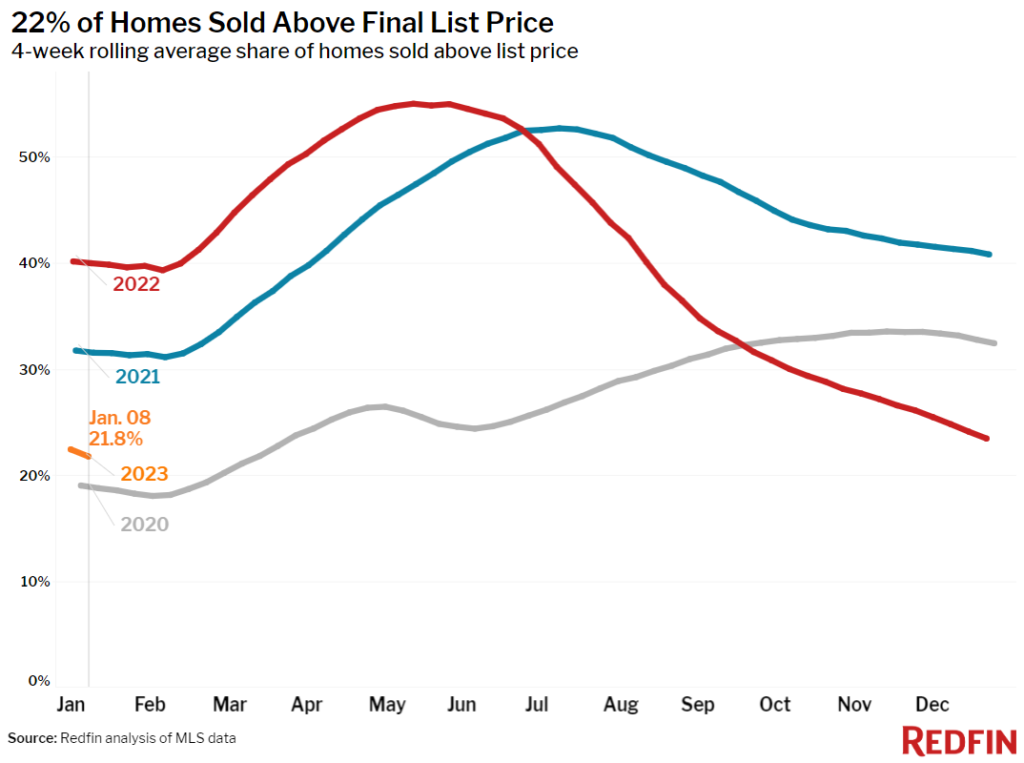

22% of homes sold above their final list price, down from 40% a year earlier and the lowest level since March 2020.

On average, 4% of homes for sale each week had a price drop, down sharply from 5.7% a month earlier.

The average sale-to-list price ratio, which measures how close homes are selling to their final asking prices, fell to 97.9% from 100.1% a year earlier. That’s the lowest level since March 2020.

Refer to our metrics definition page for explanations of all the metrics used in this report.

Source: Redfin.com